Here's the UK hiring market in one line: soft, and not turning quickly. Vacancies are at their lowest since early 2021, permanent placements are still shrinking — if more slowly than they were in the spring — and candidates are everywhere, while employers quietly move spend toward temporary staff. Every figure below is sourced to a named publisher and refreshed monthly, so you can put it in front of a client.

Is the UK recruitment market recovering in 2026?

Not yet. The headline indicators are still pointing down or sideways, and the permanent market in particular shows no sign of a quick rebound.

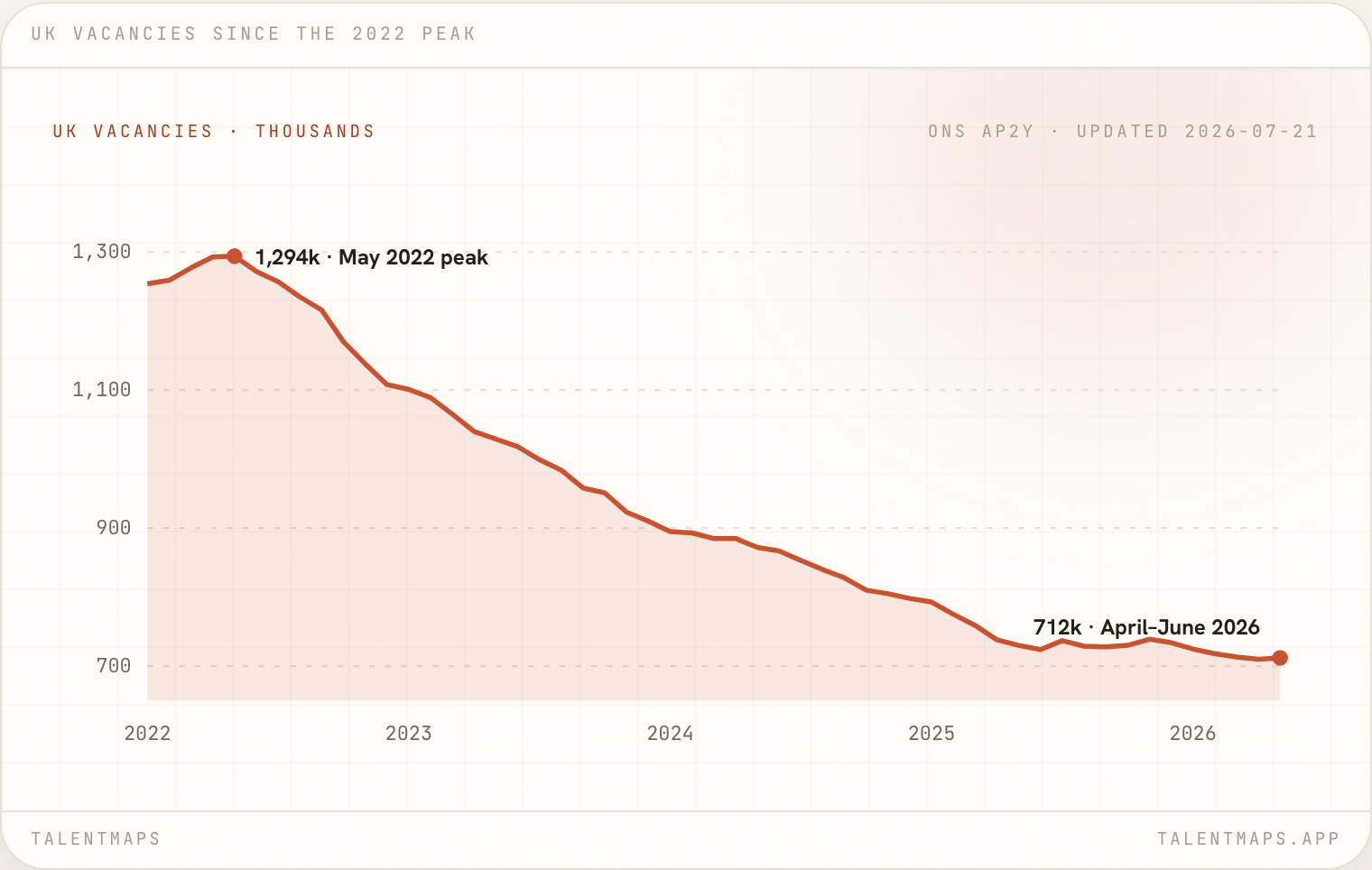

712,000

UK vacancies (April–June 2026): down 7,000 on the previous quarter and 18,000 lower than a year ago. The last time vacancies were this low was February to April 2021.

The decline is still the dominant direction, but it is no longer universal: vacancies fell in 10 of the 18 industry sectors in the ONS's latest release. Fewer open roles means the contingent model has fewer shots on goal, and more competition for each one.

{kind=link}

The shape of that line is the context for everything below: not a crash but a long, steady deflation from the 2022 hiring frenzy, now sitting below where it stood before the pandemic distorted everything.

Permanent placements

Still falling

Permanent placements fell again in June 2026, at the softest pace in three months — the closest the permanent market has come to stabilising this year. KPMG and REC publish the index level by subscription only, so the direction here is quoted from their July 2026 report rather than given as a number.

A run of declines this long isn't a blip — it's the new shape of the permanent market, and the easing in June is a slower fall rather than a recovery. Employers blame economic uncertainty and the rising cost of employment, and they keep delaying or cancelling permanent hires. Contingent fees are the revenue most exposed to this.

Temporary billings

3-year high

Temporary billings rose in June 2026 at the quickest rate since April 2023. Employers are shifting budget from permanent hires toward flexible staff.

The money hasn't vanished; it's moved. With permanent commitment feeling risky, employers buy flexibility instead. Temp billings growing at their fastest rate in over three years while permanent placements still shrink is the clearest single picture of where 2026 demand actually sits.

Candidate availability

Candidate availability rose sharply again in June 2026, driven by redundancies and softer demand — though the increase was the least pronounced in four months (KPMG & REC, July 2026).

This is the number that matters most for mapping. When candidates are scarce, your value is access. When they're everywhere — as now — access is worth little, and the value flips to judgement: which of the many available people are worth a client's time, and which of the good ones aren't on the market at all. That's what a map sells.

The wider economy

0.8–1.0%

Forecast UK GDP growth for 2026: KPMG 0.8% (down from 1.4% in 2025), the IMF 1.0%, the OECD 0.9%. Stall speed, not recession — but enough to keep employers cautious.

The labour-market signals around that growth figure point the same way. The OECD expects UK inflation to rise to 3.7% in 2026 and unemployment to reach 5.5% before both ease in 2027 (OECD). Sector by sector it's uneven: construction is in sharp contraction, with the S&P Global UK Construction PMI at 38.2 in May 2026, its weakest since May 2020 (S&P Global).

What it means for your desk

Soft demand and deep candidate supply pull one way: the value an agency adds moves from access to intelligence. When a job ad reaches the same available candidates everyone else sees, the differentiator is a deliberate read of the market — which is what a talent map is. The full down-market case is in talent mapping in a frozen market, and what to charge for a map is anchored in the UK talent mapping fee benchmark.

Sources and method

- Vacancies: ONS, Vacancies and jobs in the UK (monthly).

- Placements, billings, candidate availability: KPMG & REC, UK Report on Jobs, compiled by S&P Global (monthly).

- Macro context: KPMG European Economic Outlook, IMF Article IV, OECD Economic Outlook, S&P Global PMI.

Every number is dated to its reporting period. Where a figure is illustrative or awaiting a primary pull, it's marked as such rather than presented as fact.

Frequently asked questions

- Where does this data come from?

- Every figure on this page comes from a named primary source: the Office for National Statistics (ONS) for vacancies, the KPMG and REC UK Report on Jobs (compiled by S&P Global) for placements, billings and candidate availability, and KPMG, the IMF, the OECD and S&P Global for the wider economy. Each stat links to its source. We don't republish second-hand figures from blogs.

- How often is the snapshot updated?

- Monthly, in line with the ONS labour market release and the KPMG/REC Report on Jobs. The 'updated' date at the top shows the most recent refresh.

- Why does a talent mapping company publish hiring data?

- Because the market decides what agencies can sell. When placements are hard, the case for mapping as a paid deliverable gets stronger — and that argument only holds if it rests on real numbers rather than a sales pitch.

Written by

Joshua Aubrey · Founder, TalentMaps